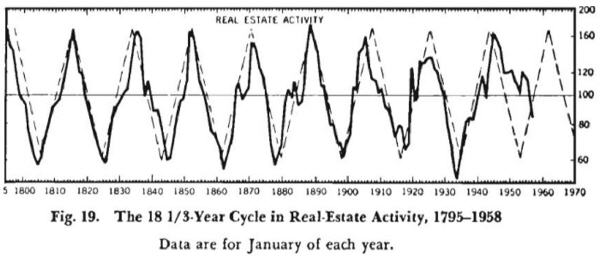

Louise McWhirter first presented her theory in her 1937 book "Astrology and Stock Market Forecasting." The model in the chart below demonstrates her claim that primary trends in business volume, finance, and stock prices are systematically delineated by the retrograde motion of the lunar North Node (NN) through the twelve signs of the zodiac.

The draconic period of the true (osculating) lunar North Node is 18.612958 years (6,798.383 days). On average,

each 30° zodiac sign is traversed in 566 days, or one year, six months, and nineteen days (1.55108 years).

each 30° zodiac sign is traversed in 566 days, or one year, six months, and nineteen days (1.55108 years).

The zodiac wheel is divided into four quadrants: "above normal," "normal," "below normal," and directional zones marked "prices up" (Leo through Libra) and "prices down" (Aquarius through Aries). Prominent arrows labeled "NODE TREND" and "TRANSITION PERIOD" indicate the clockwise retrograde flow, with gradual shifts occurring across defined transition zones near Scorpio–Sagittarius and Taurus–Gemini. Four pivotal turning points occur when the North Node enters the fixed signs, corresponding symbolically to the four heads of the cherubim in the Book of Ezekiel:

■ Aquarius represents the extreme low of business activity and the bottom of the cycle.

■ Leo signifies the extreme high of business activity and the top of the cycle.

■ Taurus marks the point at which business activity reaches a normal level while the overarching trend remains downward.

■ Scorpio indicates business activity reaching a normal level while the trend is upward.

The intervening signs provide precise transitional and amplifying effects:

► Aquarius: Extreme low of business activity, the bottom of the cycle.

► Pisces: Business activity approaches the bottom of the cycle.

► Aries: Business activity starts to fall below the normal level.

► Taurus: Business activity reaches a normal level, but the trend is going down.

► Gemini: Business continues to fall lower towards the normal level.

► Cancer: Business activity fades from the top.

► Leo: Extreme high of business activity, the top of the cycle.

► Virgo: Business activity goes even higher.

► Libra: Business activity starts to go above the normal level.

► Scorpio: Business activity reaches a normal level, and the trend is going up.

► Pisces: Business activity approaches the bottom of the cycle.

► Aries: Business activity starts to fall below the normal level.

► Taurus: Business activity reaches a normal level, but the trend is going down.

► Gemini: Business continues to fall lower towards the normal level.

► Cancer: Business activity fades from the top.

► Leo: Extreme high of business activity, the top of the cycle.

► Virgo: Business activity goes even higher.

► Libra: Business activity starts to go above the normal level.

► Scorpio: Business activity reaches a normal level, and the trend is going up.

► Sagittarius: Business continues to go higher towards the normal level.

► Capricorn: Business activity turns up from the bottom.

► Capricorn: Business activity turns up from the bottom.

These phases are not instantaneous but unfold within the broader nodal transit and transition periods shown on the wheel. The following ingress dates, drawn directly from the established nodal cycle, demonstrate the theory’s practical application across recent and forthcoming years:

► November 11, 2015: NN enters Libra.

► May 9, 2017: NN enters Virgo.

► November 6, 2018: NN enters Leo.

► May 5, 2020: NN enters Cancer.

► January 18, 2022: NN enters Gemini.

► July 17, 2023: NN enters Taurus.

► January 11, 2025: NN enters Aries.

► July 26, 2026: NN enters Pisces.

► January 27, 2028: NN enters Aquarius.

► August 2, 2029: NN enters Capricorn.

► January 26, 2031: NN enters Sagittarius.

► October 2, 2032: NN enters Scorpio.

► April 2, 2034: NN enters Libra.

► October 25, 2035: NN enters Virgo.

[The intervals reflect the variable motion of the true North Node, ranging from 542 to 623 days while averaging to the theoretical 566.532-day mean.]

As of March 2026, the North Node resides in Aries, a phase in which business activity begins to fall below the normal level within the “prices down” quadrant. This downward pressure persists until July 26, 2026, when the Node enters Pisces. Throughout the remainder of 2026 and the entire year of 2027, the Pisces transit prevails, during which business activity steadily approaches the bottom of the cycle. The subsequent ingress into Aquarius on January 27, 2028 will mark the extreme low, completing the descent that commenced in Aries.

McWhirter’s model suggests subdued business volumes, contracting financial activity, and a prevailing downward bias in prices through 2027. While this part of her theory does not specify intra-sign turning points and acknowledges that secondary factors (such as other planetary cycles or policy interventions) may modify outcomes by up to 20%, it supplies a disciplined structural overlay that contextualises shorter-term technical, fundamental, and sentiment indicators.

See also: