J.M. Hurst’s Cyclic Theory

J.M. Hurst, an American aerospace engineer, is widely regarded as the "father of modern cyclic analysis" due to his pioneering work in applying computational methods to study cyclical patterns in financial markets during the 1960s and 1970s. His innovative use of early mainframe computers to analyze price movements marked a significant departure from traditional technical analysis, establishing a systematic, scientific approach to understanding market behavior. Below is a detailed exploration of Hurst’s life, his cyclic theory, its principles, applications, and its lasting impact on technical analysis.

James Marsden Hurst (1924—2005).

The Profit Magic of Stock Transaction Timing (1970): A book that introduced his cyclic theory to a broader audience, outlining a simplified methodology for applying cyclic principles to trading.

The Cyclitec Cycles Course (also known as J.M. Hurst’s Cycles Course): A comprehensive, workshop-style course published in the early 1970s, which provided an in-depth exploration of his cyclic analysis techniques. This course, spanning over 1,500 pages, was initially distributed to a limited audience (approximately 250 copies) and later republished by Traders Press until 2012.

The Cyclitec Cycles Course (also known as J.M. Hurst’s Cycles Course): A comprehensive, workshop-style course published in the early 1970s, which provided an in-depth exploration of his cyclic analysis techniques. This course, spanning over 1,500 pages, was initially distributed to a limited audience (approximately 250 copies) and later republished by Traders Press until 2012.

Hurst claimed a 90% success rate trading on the basis of his theory, and yet the theory has remained largely undiscovered and often misunderstood. Despite his significant contributions, he remained a relatively enigmatic figure. After teaching seminars for a few years in the early 1970s, he largely withdrew from public life, and little is known about his later years. He passed away in 2005, leaving behind a legacy that continues to influence technical analysts and traders. His work gained renewed interest in 2011, when South African filmmaker and trader David Hickson used modern computing and his Sentient Trader platform to make Hurst's complex methods more accessible.

A key aspect of Hurst’s cyclic principles is that multiple cycles influence the price movements of any financial market simultaneously. Unlike other cyclic theories, Hurst’s approach emphasizes that these multiple cycles work together to shape price movements.

Another critical concept is that the cycles affecting financial markets operate continuously—24 hours a day, 7 days a week, 365 days a year—regardless of whether the market is actively trading. This continuous influence underscores the importance of understanding cycles to predict price movements accurately.

%20-%20J.%20M.%20Hurst%20Cycles%20Trading%20Course%20%5B1177%20p.%5D%20conv%2090.png)

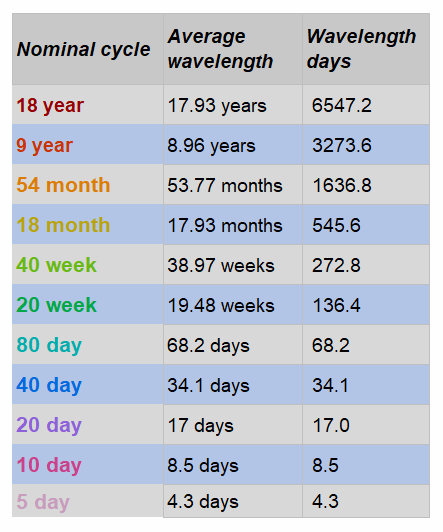

Hurst’s cycles are not a random collection of varying lengths. Instead, they are organized in what Hurst called the nominal model, a structured list of cycles with harmonically related wavelengths. For example, Hurst’s default nominal model includes cycles ranging from the 18-year cycle (with an average wavelength of 6,547.2 days, or approximately 17.93 years) down to shorter cycles, such as 5 days. In developing Sentient Trader, David Hickson extended this model to include intraday cycles as short as 3 minutes. The harmonic relationship means that the wavelength of one cycle (e.g., the 18-year cycle) is related to another (e.g., the 9-year cycle) by a simple ratio, such as 2:1.

While cycles have average wavelengths, they are not fixed. A fundamental principle of Hurst’s theory is that cycle wavelengths vary. For instance, the 18-year cycle’s average length is 17.93 years, but its actual duration may fluctuate. Understanding this variation is crucial for applying Hurst’s principles effectively in trading.

or summation cycle of the three to four most prominent cycles (red), and thus from actual market price extremes.

Core Principles

Hurst’s Cyclic Theory is based on the premise that financial market price movements are not random but are driven by a combination of harmonically related cycles. These cycles, varying in duration and amplitude, combine to produce the complex price patterns observed in markets. Hurst’s approach refutes the random walk hypothesis, which posits that price movements are unpredictable, by demonstrating that they follow ordered, quasi-predictable patterns.

His theory is grounded in eight key principles, which distinguish it from other cyclic theories:

2. Principle of Cyclicality: Price movements in financial markets consist of a combination of specific waves that exhibit cyclic characteristics. This principle implies that market behavior is driven by repetitive patterns with defined wavelengths, enabling analysts to forecast trends by identifying and decomposing these waves into their cyclic components. In practical application, this cyclicality facilitates the recognition of recurring highs and lows across various timeframes and assets, supporting strategies that align trades with the underlying rhythmic nature of price action.

3. Principle of Summation: Observed price movements in financial markets result from the additive combination of multiple cycles operating simultaneously. This principle implies that the net market trend is the sum of these overlapping cycles, where individual components contribute to the overall pattern, allowing for some randomness and interaction with fundamental factors. In practical application, this summation enables traders to deconstruct complex price data into constituent cycles, improving the accuracy of forecasts by accounting for the collective influence of short-, medium-, and long-term waves.

6. Principle of Proportionality: The amplitude of a cycle in financial markets is directly proportional to its wavelength, with longer cycles producing greater price swings than shorter ones. This principle implies that extended cycles exert a more substantial influence on overall trends, while brief cycles contribute to minor fluctuations within those trends. In practical application, this proportionality guides analysts in prioritizing dominant cycles for forecasting major movements, allowing for scaled risk management and position sizing based on the expected impact of cycle lengths.

1. Principle of Commonality: Financial markets worldwide exhibit a significant degree of shared movement in their cyclical patterns. This principle implies that troughs, and to a lesser extent peaks, tend to occur at similar times across various markets, although the magnitudes of these turning points may differ due to variations in cycle phasing, harmonic relationships, and wavelengths. In practical application, this commonality facilitates cross-market analysis, where an observable trough in one market may indicate a subtler or "hidden" equivalent in another, thereby aiding in the identification of synchronized cycle behaviors.

2. Principle of Cyclicality: Price movements in financial markets consist of a combination of specific waves that exhibit cyclic characteristics. This principle implies that market behavior is driven by repetitive patterns with defined wavelengths, enabling analysts to forecast trends by identifying and decomposing these waves into their cyclic components. In practical application, this cyclicality facilitates the recognition of recurring highs and lows across various timeframes and assets, supporting strategies that align trades with the underlying rhythmic nature of price action.

The Principle of Cyclicality.

3. Principle of Summation: Observed price movements in financial markets result from the additive combination of multiple cycles operating simultaneously. This principle implies that the net market trend is the sum of these overlapping cycles, where individual components contribute to the overall pattern, allowing for some randomness and interaction with fundamental factors. In practical application, this summation enables traders to deconstruct complex price data into constituent cycles, improving the accuracy of forecasts by accounting for the collective influence of short-, medium-, and long-term waves.

4. Principle of Harmonicity: Wavelengths of cycles in financial markets are interrelated by small integer ratios, typically harmonics such as 2:1 or occasionally 3:1. This principle implies that cycles form a nested, proportional structure, where shorter cycles are subdivisions of longer ones, creating alignment across different timeframes. In practical application, this harmonicity aids in predicting market movements by identifying these ratio-based relationships, allowing analysts to scale cycle analysis from intraday to multi-year periods while anticipating synchronized turning points.

The Principles of Harmonicity & Synchronicity.

5. Principle of Synchronicity: Cycle troughs in financial markets tend to align and occur simultaneously when possible, particularly across cycles of different magnitudes. This principle implies that major market lows often coincide due to this synchronization, distinguishing it from other cyclic theories by emphasizing trough convergence over random phasing. In practical application, this synchronicity facilitates the identification of significant turning points, enabling traders to confirm cycle lows through multi-cycle alignment and enhance timing for entries or exits in various markets.

6. Principle of Proportionality: The amplitude of a cycle in financial markets is directly proportional to its wavelength, with longer cycles producing greater price swings than shorter ones. This principle implies that extended cycles exert a more substantial influence on overall trends, while brief cycles contribute to minor fluctuations within those trends. In practical application, this proportionality guides analysts in prioritizing dominant cycles for forecasting major movements, allowing for scaled risk management and position sizing based on the expected impact of cycle lengths.

7. Principle of Nominality: Financial markets adhere to a set of nominal, or average, cycle lengths derived from historical observations, forming a standardized model for analysis. This principle implies that while actual cycles may vary, these nominal wavelengths provide a consistent baseline for categorizing and comparing cyclic behavior across assets. In practical application, this nominality supports the development of cycle hierarchies, enabling traders to apply a uniform framework to identify and project cycle phases despite market-specific deviations.

The Principle of Nominality.

8. Principle of Variation: Actual cycle lengths and amplitudes in financial markets deviate around their nominal values due to inherent market dynamics and external influences. This principle implies that while cycles follow general patterns, flexibility is required to account for these variations, preventing rigid application of the nominal model. In practical application, this variation encourages adaptive analysis techniques, such as phasing adjustments, to refine forecasts and accommodate real-time shifts in cycle behavior across different instruments and conditions.

54 Month Cycle = 3 x 18 Month Cycle = 6 x 40 Week Cycle (9 Month Cycle) = 12 x 20 Week Cycle

= 24 x 80 Day Cycle = 48 x 40 Day Cycle = 96 x 20 Day Cycle = 192 x 10 Day Cycle = 384 x 5 Day Cycle

The 54-month cycle, made up of three 18-month cycles, marks the midpoint of the 9-year cycle, which is half of the 18-year cycle.

Hurst's nominal model as a series of sinusoids and summed to create the black 'composite model.' Here the orange line is the 18 month cycle, the light green the 40 week cycle, dark green the 20 week component, light blue the 80 day component, dark blue the 40 day component and finally the 20 day cycle is the purple sinusoid. The X axis represents the number of days.

The 54-month cycle and its subdivisions.

.jpg)

The 18-month cycle composed of a bullish 9-month cycle phase and a bearish 9-month cycle phase.

18-Month Cycle Projection for the S&P 500 based on Hurst's Nominal Model.

Projection for the S&P 500 during the bullish 9-month cycle phase of the 18-Month Cycle.

The Nominal Model

Hurst’s research identified a set of nominal cycles that he believed were common across financial markets. These cycles are harmonically related and form the basis for his analysis. A simplified version of his nominal cycle model, as extended by later researchers like David Hickson, includes:

These cycles are related by small integer ratios (e.g., a 20-day cycle is twice a 10-day cycle, and a 54-month cycle is three times an 18-month cycle). This harmonic structure allows analysts to break down price movements into their constituent cycles and predict future price action based on their interactions.

5-day cycle (≈ 4.3 days)

10-day cycle (≈ 8.5 days or 1.25 weeks)

20-day cycle (≈ 17 days or 2.5 weeks)

40-day cycle (≈ 34.1 days or 5 weeks)

80-day cycle (≈ 68.2 days or 10 weeks)

20-week cycle (≈ 136.4 days or 19.97 weeks or 4.5 months)

40-week cycle (≈ 272.8 days or 38.97 weeks or 9 months)

18-month cycle (≈ 17.93 months)

54-month cycle (≈ 4.5 years)

9-year cycle (≈ 8.96 years)

18-year cycle (≈ 17.93 years)

10-day cycle (≈ 8.5 days or 1.25 weeks)

20-day cycle (≈ 17 days or 2.5 weeks)

40-day cycle (≈ 34.1 days or 5 weeks)

80-day cycle (≈ 68.2 days or 10 weeks)

20-week cycle (≈ 136.4 days or 19.97 weeks or 4.5 months)

40-week cycle (≈ 272.8 days or 38.97 weeks or 9 months)

18-month cycle (≈ 17.93 months)

54-month cycle (≈ 4.5 years)

9-year cycle (≈ 8.96 years)

18-year cycle (≈ 17.93 years)

These cycles are related by small integer ratios (e.g., a 20-day cycle is twice a 10-day cycle, and a 54-month cycle is three times an 18-month cycle). This harmonic structure allows analysts to break down price movements into their constituent cycles and predict future price action based on their interactions.

Nominal Cycle vs Average Cycle or Wavelength.

%20-%20Hurst%20Method%20Nominal%20Market%20Cycle%20Chart.png)

Hurst Method Nominal Market Cycle Chart by Richard Russell, Dow Theory Letters, 1985.

40-Week Cycle with bearish trend.

The addition of an underlying trend impacts the summary status

of each interaction in the series, influencing decisions.

of each interaction in the series, influencing decisions.

- The longest cycle identified in this model spans 54 years, followed by an 18-year cycle, and the shortest at this level is 9 years. For Hurst's cycle analysis, these are considered very long-term trends.

- On a monthly scale, the 9-year cycle breaks down into two 54-month cycles, which further split into three 18-month cycles (often referred to as 80 weeks), and then into two nine-month cycles.

- The nine-month cycle corresponds to a 40-week cycle, consisting of two 20-week cycles that further divide into two 10-week cycles.

- The 10-week cycle is represented as an 80-day cycle on daily charts, which breaks down into 40-day, 20-day, and 10-day cycles.

- Additionally, cycles exist that are longer than 54 years and shorter than 10 days.

Note

that e.g. a so called 20-day cycle low can occur several days before or

after the expected 20 days from the previous low, which may also have

occurred several days outside its ideal timeframe. The 20-day cycle,

based on spectral or other analyses, might actually be 19.2 days or 20.4

days. Consequently, cycle periods are indefinite and carry a margin of

error. For investment purposes, this means all cycles should be regarded

as guides. Even the well-established seasonal cycle has actual high and

low dates that can vary significantly from year to year.

Key Tools and Techniques

Hurst developed several tools and techniques to apply his cyclic theory to trading and investing. These include:

2. Valid Trend Lines (VTLs): VTLs are drawn by connecting the troughs of two recent cycles of the same degree and extending the line forward. A price crossing below a VTL confirms a peak in a cycle of a higher degree, helping traders validate cycle placement and anticipate reversals.

1.

Phasing Analysis: This involves identifying the phase (trough, peak, or

in-between) of each cycle influencing the market. By analyzing

historical price data, traders can determine the timing and magnitude of

cycles to predict future price movements. Phasing analysis is central

to Hurst’s methodology and is described as a combination of science and

art.

2. Valid Trend Lines (VTLs): VTLs are drawn by connecting the troughs of two recent cycles of the same degree and extending the line forward. A price crossing below a VTL confirms a peak in a cycle of a higher degree, helping traders validate cycle placement and anticipate reversals.

3.

Future Lines of Demarcation (FLDs): FLDs are projections of past cycle

troughs shifted forward by the wavelength of a specific cycle. They

serve as dynamic support and resistance levels, helping traders identify

potential price reversal points. For example, if a 20-day cycle trough

is projected forward, the FLD can indicate where the next trough or peak

might

occur.

4.

Channel and Envelope Analysis: Hurst used channels and envelopes to

visualize cycle-driven price movements. Channels are formed by drawing

parallel lines around price action, capturing the cyclical swings, while

envelopes smooth the price data to highlight dominant cycles. These

tools aid in forecasting price targets and

reversals.

5.

Cycle-Based Trading Strategies: Hurst’s methodology emphasizes timing

trades based on cycle troughs and peaks. For example, buying at a trough

of a shorter cycle (e.g., 20 days) when supported by a longer cycle

(e.g., 80 days) can lead to high-probability trades. His approach also

includes risk management and position sizing, as seen in modern tools

like the OddsTrader app.

.png)

Note: Hurst's average wavelengths can contract and expand significantly (± 10-15%).

Hurst’s Nominal Model is based on calendar time and not trading time, which presents a slight problem for anyone using a trading platform set up only to show trading days, which of course means pretty much everyone. The following conversion therefore needs to be made at the daily level:

- There are roughly 250 trading days in a 365-day calendar year. To convert calendar days to trading days, therefore, multiply by 0.7 (250/365).

- Conversely, to convert trading days into calendar days, divide by 0.7 (multiply by 1.42).

- Thus, the nominal 80-day cycle is 80 x 0.7, or 56 trading days.

- The nominal 40-day cycle is 40 x 0.7, or 28 trading days.

- The nominal 20-day cycle is 20 x 0.7, or 14 trading days, and so on.

These numbers should be familiar to most technicians as the basis for the popular 55-day moving average; the 26-day standard setting for MACD; and the 14-day default settings for RSI, DMI and Stochastics.

There are numerous enthusiastic advocates—prominent traders and writers—who proclaim Hurst as the “father of cyclic analysis” and attest to the effectiveness of his theory (including the late Brian Millard, who authored several books on the subject). Yet, why isn’t the theory better known or more widely used by technical analysts? There are two main reasons:

Firstly, Hurst’s Cyclic Theory is not “easy.” While it is beautifully simple and elegant in essence, it is neither easy to understand nor straightforward to apply. "The Cycles Course" spans over 1,500 pages, and most readers take several months to work through it.

Secondly, although the theory presented in both "Profit Magic" and "The Cycles Course" is the same at its core, there is a critically important distinction between the analytical processes outlined in each. Hurst attributed his success to the method presented in "The Cycles Course", yet many readers stop at "Profit Magic" and go no further—consequently, they never discover the more effective process found in the course.

Secondly, although the theory presented in both "Profit Magic" and "The Cycles Course" is the same at its core, there is a critically important distinction between the analytical processes outlined in each. Hurst attributed his success to the method presented in "The Cycles Course", yet many readers stop at "Profit Magic" and go no further—consequently, they never discover the more effective process found in the course.

Christopher Grafton’s book, Mastering Hurst Cycle Analysis (2011), modernized Hurst’s methods by providing code for indicators in programming languages, making them easier to implement on modern trading platforms. Grafton’s work includes over 120 color charts and practical examples, bridging the gap between Hurst’s complex theory and today’s traders.

The 9-Month Cycle

The most important cycle in market analysis is the 9-Month Cycle, also known as the 40-Week Cycle, 39-Week Cycle, or 8.6-Month Cycle. Many traders and analysts utilize this cycle because it is critical for intermediate-term market forecasting. It helps in planning for and identifying significant declines and rallies throughout the year. Even short-term traders should monitor the 9-Month Cycle to remain aligned with the broader trend.

.png)

The structure of the 9-Month Cycle consists of two 20-Week Cycles, referred to as Phase 1 and Phase 2. Each 20-Week Cycle is further divided into two 10-Week Cycles, also labeled Phase 1 and Phase 2.

Typically, the most powerful rally within the 9-Month Cycle occurs during the first three months,

as all three nesting cycles align to produce upward momentum.

Conversely, the market is most vulnerable to significant declines during

the last three months, when all three cycles trend downward.

In a bull market, the crest of the 9-Month Cycle generally occurs between the sixth and eighth month (right translation), while in a bear market, it is expected between the second and third month (left translation).

In addition to the crest of the 9-Month Cycle, the completion of the Phase 1 20-Week Cycle is another significant event. In a bull market, this often leads to a minor price correction or consolidation, whereas in a bear market, it likely coincides with the cycle crest.

Understanding the basic structure of the 9-Month Cycle reveals that the lowest risk for establishing new long positions typically occurs during the first three months, while the greatest risk of decline arises in the final three months. The middle three months require caution, as the Phase 1 20-Week Cycle may roll over into a trough—presenting both risks and opportunities with the onset of the Phase 2 20-Week Cycle.

Markets Are Never Flat. Underlying Trend: Sigma-L

A simple concept, but one which must be considered for our purposes as Hurstonians, is underlying trend. Named by Hurst as ‘sigma-l’

to simply mean ‘the sum of all cycles’, it is inherent in a system

which assumes cycles form an infinite series of increasing period. This

underlying trend (which can be thought of as a sum of sinusoidal

functions) is never static. It may appear to be flat when shorter cycles

form sideways consolidations but this is just a result of a much larger

period cycle, relative to the cycle in focus, turning up or down.

Traditional

technical analysis has come to love the simple moving average as an

indicator of trend, usually set at a arbitrary period of 50, 100 or 200

to smooth higher frequencies. This is a blunt tool and flawed. Firstly

by the fact moving averages must be time shifted by the (period/2) to

account for the digital filter lag and, secondly, the moving average

makes no attempt to decompose the signal, save for it’s low pass

characteristics.

In the Cyclitec cycles course Hurst

tabulated sigma-l by assessing the phase of each component in question

and arriving at an estimation for sigma-l. Below is an example of this

in Sentient Trader using the daily phasing of Bitcoin.

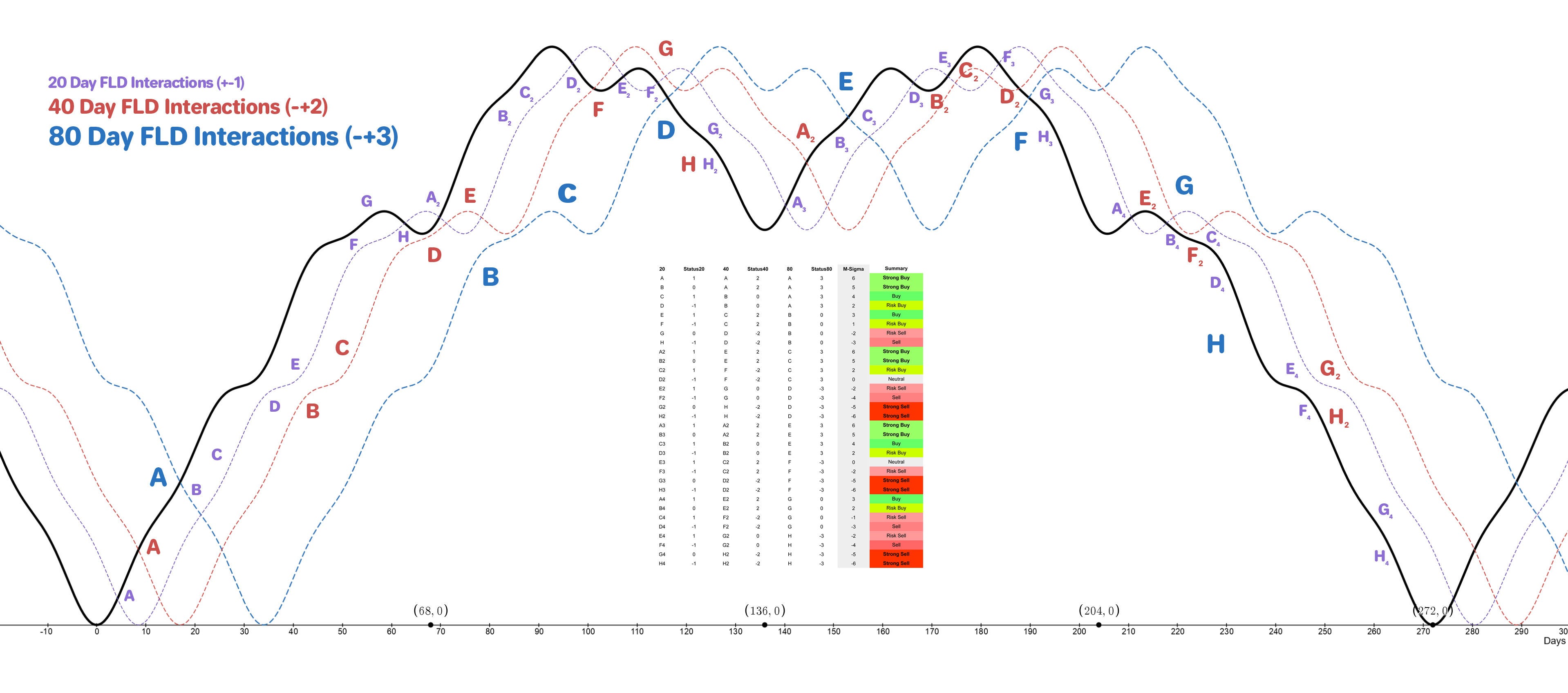

In Practice

We will take our advanced FLD trading strategy

which uses three discrete components of the nominal model and their

respective signal cycle FLDs to demonstrate a rudimentary application of

sigma-l. In this example we will assign a linear trend to the model and

observe the effect on price, interactions and the summary status of

‘M-Sigma’ - our subset of underlying trend only applicable to this 40

week sample.

In real markets the trend is not linear and is the sum of what can be thought of as discrete, sinusoidal functions of increasing wavelength.

Trend is Up

Here we assign sigma-l

a value of 1 and the dotted line below price is an indicator of it’s

function. The effect on the composite price line is obvious with the

familiar ‘higher low’ forming at the end of the chart and price skewed

upwards.

Trend is Down

Here we assign sigma-l

a value of -1 and the inverse effect of a positive sigma-l is observed.

The effect on the composite price line a ‘lower low’ forming at the end

of the chart and price skewed downwards.

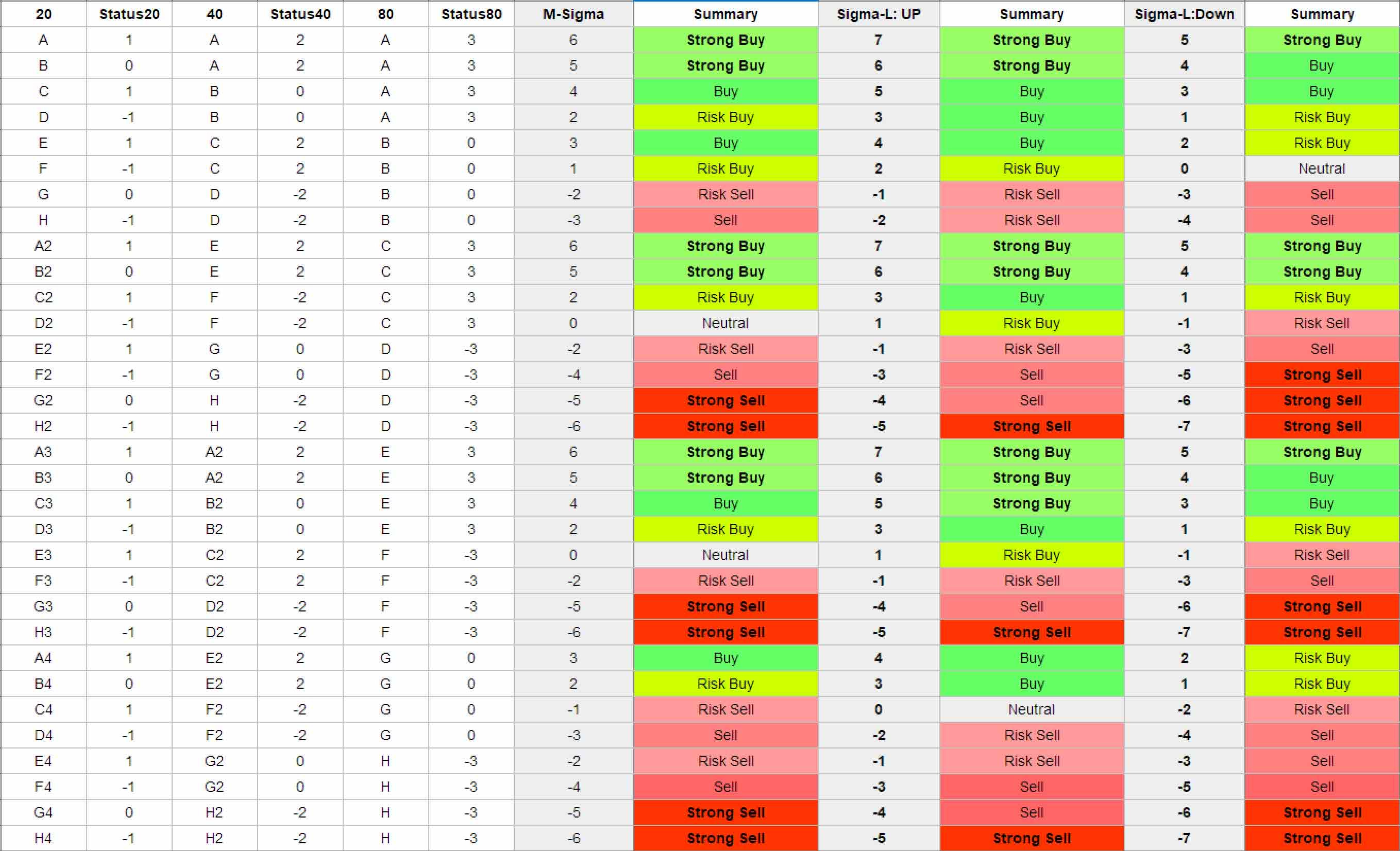

We can now look at what effect the addition of this simple linear trend has on our overall summary at each 20 day FLD interaction and the strength of the trade associated with it.

The

tabulation above shows the summary of each 20 day FLD interaction in

the idealised 40 week period, via the model described previously. M-Sigma

shows interaction trade direction and strength when the underlying

trend is assumed to be 0, essentially a localised subset of underlying

trend. Subsequent summary columns show the resulting

differences when underlying trend is up and down, respectively, as a

true reflection of Sigma-L. This more closely resembles real price action in financial markets.

Looking at the summary columns with underlying trend accounted for we can see that in the bullish scenario, those trends previously described as ‘risk buy’ are now standard ‘buys’, some ‘buys’ become ‘strong buys’ and so on. The underlying trend has the effect of amplifying bullish signals and attenuating bearish signals. Of course the inverse is true when the underlying trend is bearish.

Reference: