The Economic Confidence Model that I discovered back in the 1970s was not based on any particular market or economy. It was devised by taking a list of world panics in the economy, irrespective of where they began, utilizing a list of 26 events between 1683 and 1907. It was dividing 26 into the 224 year time period that produced the basic frequency of 8.615384615.

Big Fish Eat Little Fish - Pieter Bruegel the Elder, 1556.

Like Adam Smith, I set out upon a course of observation to try to understand what made a cycle even exist. Through the course of my studies of the past and observations of the present, I came to realize that the observations uncovered a rich and dynamic structure of interactivity between mankind himself, as well as nature from weather to earthquakes. In short, what scientists were just then discovering with the aid of computers that could do millions of calculations impossible by hand, that the image of chaos has been completely altered. What may appear to be chaos, is in reality, only complex interaction that can be observed by only pealing back layers upon layers like an onion.

|

Written by Martin Armstrong on a type-writer while imprisioned in FCI, Fort Dix, New Jersey, 2009.

|

[...] Now that we understand what makes one economy boom against all others, or a particular sector within an economy because Capital Concentrates, now we can look at the ECM with the proper perspective. This is a global model of economic activity that highlights the raw fact that man will speculate no matter what and that creates the Capital Concentration. The ECM gives us the perspective of short-term business cycle movements at the 8.615384615 year level, but this frequency moved both up and down in time in layers like an onion. It builds into groups of 6 waves forming a 51.6 year major cyclical wave where confidence between the people and the state alternate at the generational level. This builds into 6 waves again of 51.6 years into 309.6 year waves upon which nations rise and fall.

[...] There are those who no matter what you show them or what you say they will never believe in cycles. For those of us who do, we need that disbelief to trade against. There always has to be two sides to a coin, as well as a market.

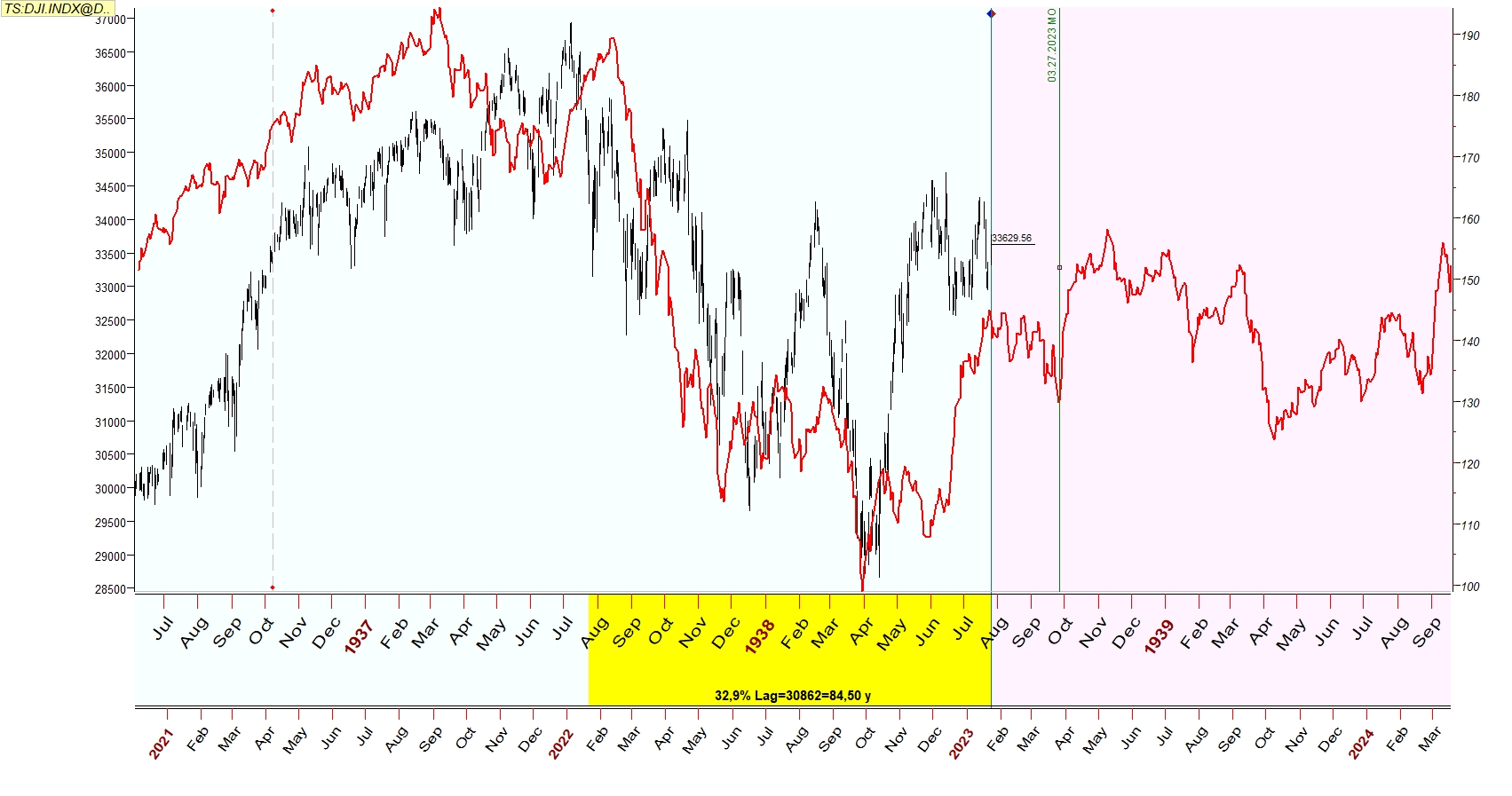

[...] Look a major collapses from all bubble tops and this is what you will find. The minimum amount of time to complete the fall and decline is this 31-34 month time period except in the Waterfall Events.

[...] There has been a lot written about the Science of Chaos. The true person to develop this field was B. Mandelbrot. The science of chaos that produced the fractal geometry I regard from a pure economic perspective as a proof of the existence of layers upon layers, but it offers no predictive value for our real economy in the traditional sense.

[...] What fractal geometry demonstrates is that there is no real just chaos, just such degree of complexity that our eye has been unable to see the complex order. Fractal Geometry and its insights is based upon Complex Numbers. For those who do not remember the school days, unlike all other numbers, the Complex Numbers do not exist on a horizontal plane. The Natural Numbers 1 through 9, for example, can be plotted on a horizontal line.

[...] Unlike Natural Numbers, Complex Numbers do not exist on a horizontal line. They exist only on an x-y coordinate time plane where Natural Numbers and Regular Numbers on a horizontal grid combine into what we call Imaginary Numbers on the vertical grid. These Imaginary Numbers are simply numbers where taking a negative number times another negative number produces a negative instead of a positive number, i.e. -2 * -2 = -4.

[...] We can see from the above illustration of the Economic Confidence Model that there has always been a delicate dance between the effects that follow the path of “time” as the Fourth Dimension adds to the basic equation What-How-Where with the fourth variable “When” and now we have the hidden complex field behind everything that adds the next portion to the equation “Why” that can be explained only by the Fifth Dimension of complex interaction through the process of “self-referral” that allows history to repeat. We are getting closer to the real causes and effects that have tormented mankind and often caused such hardship by the attribution of normal events to the folly of gods.

See also: