Mark Fisher is no ordinary trader. The ACD trading system (an opening range breakout concept) he described in his 2002 book The Logical Trader is the one he and his 75-plus traders at MBF Clearing Corp. still use to make a living on the New York markets day in and day out. Does it work? Ask anyone at Fisher's firm, and they'll tell you it does. Unlike many in the business of helping traders, Fisher is happy to share his system because he believes the more people there are using it, the more effective it will be. However, the following is not specifically about Fisher's ACD system, but about his Three-Day Rolling Pivot concept (from the same book) and the general function of balance levels in daily and weekly market maker templates, about the market maker algorithm, and the origins and basic rationale of short-term trading. The 'rolling pivot' is an extension of Fisher's pivot range concept.

In the charts above a Six-Day Moving Average defines a mathematically exact balance level for all segments of the weekly and daily market maker cycles. The same is true for the balance levels defined by Fisher's Three Day Rolling Pivot, by the Weekly Pivot and by the Daily Pivot. All four govern market structure and

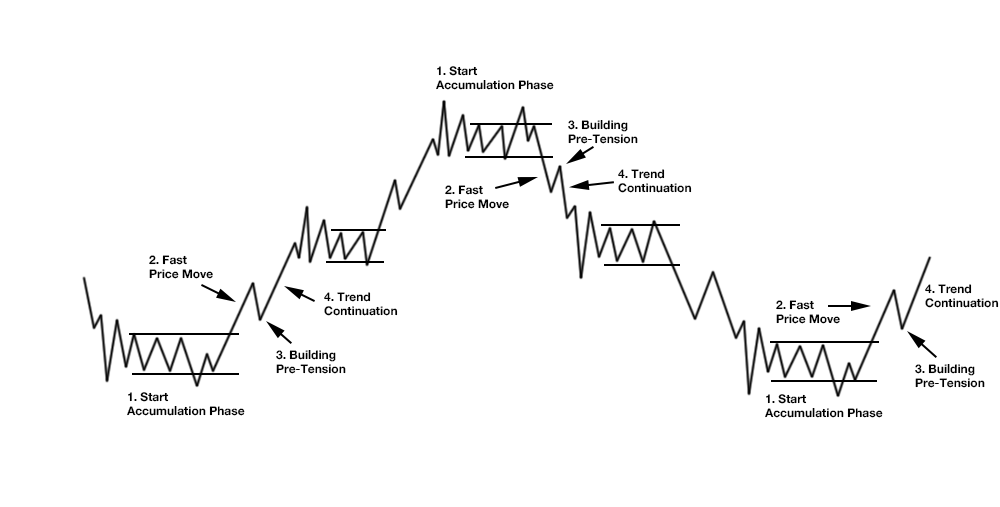

price action within and between the trading days inside the weekly cycle. Balance levels, market structure and price action reflect the market maker logic and the process of auctioning the order flow. These balance levels can be utilized in many ways, such as to determine entry points, stops and trailing stops. Is the current price out of balance, what is the distance towards these balance levels? Price is always being moved between 'liquidity pools' and (re-) balance levels. Across hours, sessions, days and weeks the market maker orchestrates the exact same eternal recurrence of the accumulation-expansion-distribution-retracement-cycle between round numbers or levels (e.g. 0, 25, 50, 75; 0, 10, 20, 30 or 0, 20, 40, 50) also known as the pump & dump cycle.

|

| 3 Bar Patterns - the smallest fractals of market structure. Inside bars are ignored, the last bar of a fractal becomes the first of the next. Where are the round number levels, the breakout levels, liquidity, the balance levels? |

Identify in the above charts day-trading, short-term trading and swing trading setups. Define price targets, entry-, exit-, stop-levels, profit/loss ratios. Be sure everything is logically solid and proportionally related to daily and weekly highs and lows and the balance levels.

|

| » All my life I've been a 60/40 player, content to clear my 20%. « - Jesse Livermore |

|

| Programming the Livermore Market Key |

Richard D. Wyckoff's Composite Operator a.k.a. Market Maker a.k.a Broker manages the order flow of 'buyers' and 'sellers' with a price generating auction algorithm realizing the highest mathematically possible return in 'dealing' with the flow of orders. Later on in life Wyckoff became a broker and market maker himself. His schematics and Jesse Livermore's tables illustrate the complete logic and algebra of the market maker's auction process and the pump & dump cycle. The auction algorithm works ever since it was invented. Livermore was able to do the math without calculator, paper and charts. Aged fourteen he started as a quotation board boy at a Boston brokerage business and literally saw patterns in the waves of numbers flowing each day from the ticker tape. Livermore came to understand that scheme generates more profit than any other business activity ever known to man. Fifteen year old Wyckoff had also begun as a broker’s runner to soon experience the exact same epiphany. Market makers were tremendously successful in multiplying their returns with the invention of electronic exchanges and with the invention of the daily global scheme between the 'Asian Session', the 'London Session', and the 'New York Session'. Wyckoff, Livermore and W.D. Gann were contemporaries, trading the same commodities, stocks and indices in the same exchanges. All were initiated into the auction algorithm. Wyckoff and Livermore were larger-than-life traders while Gann's true returns have always been subject of debates. He sold many expensive courses and forecasts. And what he sold to subscribers and students and how he actually traded for a living were very different things: Gann traded a double-tops-and-double-lows-in-the-direction-of-the-daily-trend-strategy - plain and simple pump & dump trading Wyckoff-Livermore style. What should we learn from all this? Maybe the lesson is to keep things as simple as possible as Tom Hougaard suggested.

|

| Market maker pump & dump levels. |

The accumulated length of the intraday price swings in the 1-minute chart of any instrument exceeds the daily true range several dozen times every single day. Imagine the factor on sub-1 minute time frames without having to deal with slippage nor transaction costs. Let that sink in. How is that possible? Understand the opening range concept and the logic and purpose of 'breakouts' and 'false breakouts' from that range. Monday's high and low define the opening range for the week; the high and low during the first thirty minutes the opening range of a session; the first three trading days of a new quarter limit the quarterly opening range; and the range of the first trading week of the year becomes the yearly opening range. Know the logic, principles and precision of price action and of market structure as taught nowadays e.g. by ICT or Stacey Burke: Price moving in one direction always creates the exact same imbalance on the opposite side. Imbalances are re-balanced by retracements of at least 50%. Price expands in proportions of 1/8ths or 1:1, 2:1, 3:1 etc. Price is always timed and measured and moves across all times frames always proportionately to the above listed opening ranges towards (re-) balance levels. Three and nine minutes are fractals within the hour; three hours a fractal within a session and the trading day; three and nine trading days are fractals within and across weeks; three and nine weeks fractals within months and quarters. Ideally Wednesdays and Fridays are timed for ending and re-starting three day fractals within the weekly market maker template.

Calculation of the Three-Day Rolling Pivot:

Three-Day Rolling Pivot Price = (three-day high + three-day low + close) / 3

Second number = (three-day high + three-day low) / 2

Pivot differential = daily pivot price – second number

Three-Day Rolling Pivot Range High = daily pivot price + pivot differential [omitted in above charts]

Three-Day Rolling Pivot Range Low = daily pivot price – pivot differential [omitted in above charts]

|

| The Probabilistic Mindset of Successful Traders - Mark Douglas |

Reference:

Mark B. Fisher (2002) - The Logical Trader: Applying a Method to the Madness.

|

| Mark B. Fisher |

%20-%20Price%20and%20Market%20Structures%20-%20Summary%20%5B2%20p.%5D-1.png)

%20-%20Price%20and%20Market%20Structures%20-%20Summary%20%5B2%20p.%5D-2.png)