|

| This methodology does not predict the magnitude of swings. |

Saturday, January 30, 2016

Wilshire 5000 Total Market Index vs 4 Lunar Month Cycle

Wednesday, January 27, 2016

The Periodic Table of Commodity Returns

|

| U.S. Global Investors (Jan 27, 2016) - This table shows the ebb and flow of commodity prices over the past decade. |

Thursday, January 21, 2016

SoLunar Map February - March 2016

|

| This

chart depicts the solunar bias for short-term movements of stock

indices two months ahead. The markets are certainly influenced also by other planetary forces - especially longer-term - but a 3-5 day short-term rhythm and pattern is governed by the solunar forces (= 4 highs and 4 lows per lunar month). The solunar forces are a composite of Sun-Moon angles, orbital eccentricities, declinations and some long-term cycles. A Low in the SoLunar Map frequently is a High in the stock market and vice versa. Inversions occur, and if so, they should occur only once every 4 lunar months around a New Moon (max +/- 7 days). The solunar rhythm is frequently disturbed by (1.) the FED, and (2.) by sudden solar activity, altering the geomagnetic field, and hence the mass mood. This can result in the skip and/or inversion of pivots in the SoLunar Map. An increasing number of sunspots and flares have usually a negative influence on the stock market some 48 hours later, and vice versa (Ap values > 10 are usually short-term negative). A rising blue line in the SoLunar Map means the bias for the market is side-ways-to-up, and vice versa. Highs and lows in the SoLunar Map also may coincide with the start and termination of complex, side-ways correction patterns like zig-zags, triangles or flags. Upcoming turn-days are: Jan 28 (Thu), Feb 01 (Mon), Feb 04 (Thu), Feb 08 (Mon), Feb 11 (Thu), Feb 15 (Mon), Feb 26 (Fri), Mar 01 (Tue), Mar 05 (Sat), Mar 08 (Tue), Mar 12 (Sat), Mar 16 (Wed), Mar 19 (Sat), Mar 23 (Wed), Mar 27 (Sun), Mar 30 (Wed), Apr 03 (Sun). Cross check these dates with the Cosmic Cluster Days, the Bradley Indices, and Jack Gillen's Sensitive Degrees. Previous SoLunar Maps HERE |

|

| Please note: since around Jan 13th the correlation flipped = now Low in the SoLunar Map is Low in the SPX; a High in the etc. |

Cosmic Cluster Days in February - March 2016

|

| The basic assumption here is that heliocentric and geocentric angles between planets are related to financial market movements. A signal is triggered when the composite line of all aspects breaks above or below the Average Cosmic Noise Channel. Upcoming Cosmic Cluster Days (CCDs) are: Jan 24 (Sun), Feb 07 (Sun), Feb 09 (Tue), Feb 18 (Thu), Feb 22 (Mon), Mar 03 (Thu), Mar 10 (Thu), Mar 23 (Wed), Mar 28 (Mon), Mar 30 (Wed), Apr 04 (Mon). Previous CCDs are HERE |

Wednesday, January 20, 2016

Tuesday, January 19, 2016

Monday, January 18, 2016

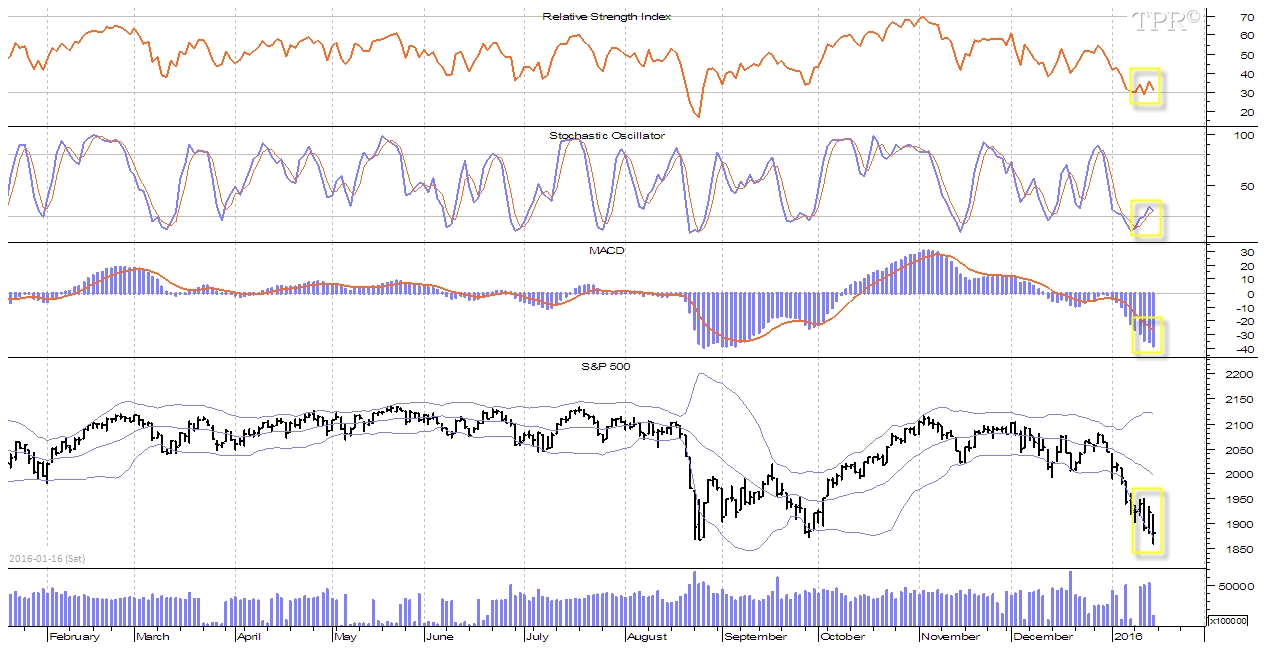

Saturday, January 16, 2016

Breakeaven Oil Price - Towards The Collapse Of Saudi Arabia

|

| Costs of Oil Production 2015 - Enlarge (Credits: Aargam) |

|

| HERE |

Friday, January 8, 2016

DJIA In 4th Longest Bull Market Since 1900 - UBS: Sell Stocks, Buy Gold!

[...] As of 2017, gold could profit from the US dollar moving in a major top and starting a bear market [...] In 2015, the bounce in gold was weaker than expected. However, in all these cases we made it clear that we just expect a bear market rally before resuming its dominant cyclical bear trend. Generally, our cyclical roadmap and our long-term call on gold of the last few years has not changed. A potential bottom in 2016 bottom could be a rather powerful bottom, since together with a four-year cycle low we have also an eight-year cycle low projection for this year. In this context we expect a potential 2016 low in gold to be the basis of a new multi-year bull market. Source: UBS (Jan 06, 2016)

Tuesday, January 5, 2016

{kind=link}

2016 - Presidential Cycle - Seasonal Cycle - Decennial Cycle of DJIA

Since 1834 the U.S.-stock market has been positive 10 (56%) out of 18 times in the 6th year of every decade, and the average annual gain of a 6th year was 3.74%. Since the 1970s the DJIA gained 16% to 26% during the 6th year of each decade. On average the DJIA's 6th year in the Decennial Cycle, the Annual or Seasonal Cycle and the Presidential Cycle are all positive. In the average Decennial Cycle the DJIA scores the Low of the 6th Year in late January, rises into mid July, drops into September, before surging for the rest of the year. The Presidential Cycle drops from an early January High to a late February Low, rises into early April, drops to late May, rises again into early September, drops to early October before rising into the year-end.

|

| Credits: Seasonal Charts |

|

| Credits: www.realinvestmentadvice.com |

Monday, January 4, 2016

When Not To Put Money In The Bank - Negative Interest Rates in Europe

European Central Bank -0.3%

Swiss National Bank -0.75%;

Danish Central bank -0.75%

Swedish Central Bank -1.1%

Swiss National Bank -0.75%;

Danish Central bank -0.75%

Swedish Central Bank -1.1%

Why are they in negative territory? For all these countries it is the exchange rate against the Euro

that is important. Negative interest rates weaken a country’s currency

and make imports more expensive and exports cheaper. Furthermore central

banks could be trying to prevent a slide into deflation, or a spiral of

falling prices that could derail the recovery.

In

theory, interest rates below zero should reduce borrowing costs for

companies and households, driving demand for loans. In practice, there’s

a risk that the policy might do more harm than good. If banks make more

customers pay to hold their money, cash may go under the mattress

instead. Janet Yellen, the U.S. Federal Reserve chair, said at her

confirmation hearing in November 2013 that even a deposit rate that’s

positive but close to zero could disrupt the money markets that help

fund financial institutions. Two years later, she said that a change in

economic circumstances could put negative rates “on the table” in the

U.S., and Bank of England Governor Mark Carney said he could now cut the

benchmark rate below the current 0.5 percent if necessary. Deutsche

Bank economists note that negative rates haven’t sparked the bank runs

or cash hoarding some had feared, in part because banks haven’t passed

them on to their customers. But there’s still a worry that when banks

absorb the cost themselves, it squeezes the profit margin between their

lending and deposit rates, and might make them even less willing to

lend. Ever-lower rates also fuel concern that countries are engaged in a

currency war of competitive devaluations. Source: Bloomberg

Subscribe to:

Posts (Atom)